Scotland’s massive sea area contains at least £1 trillion of energy wealth

It’s facts not fear that will win the referendum debate. This is especially important when discussing the future of Scotland’s offshore revenue.

Scotland has a strong and diverse economy with many strengths, and the energy sector is an important part of this.

However, across the past four decades governments in Westminster have played down or even hidden the evidence of great wealth in Scotland’s sea bed. Evidence has gradually emerged to this effect, especially online.

– Professor Sir Donald MacKay accused the UK Government of ignoring “a mountain of black gold”.

– Westminster took an absurd position on North Sea oil

– An independent Scotland will benefit from better exploration techniques

– 10 key facts on Scotland’s oil and independence

– Bank of Scotland: 39,000 jobs to be created in oil and gas sector

– Scotland on the verge of new North Sea oil boom

These reports within the last year sit alongside the cover-up of the McCrone report, the admission by former Chancellor Denis Healey that offshore revenues were hidden from Scotland, and reports last week from Investors Chronicle that Westminster was once again underplaying the value of oil in the run-up to the referendum.

This has focused attention on the future of the sector, especially in light of David Cameron’s strangely under-publicised visit to Shetland.

The Clair Ridge Field

Off the West coast of Shetland is the Clair Ridge field. It contains an estimated 8 billion barrels of oil, with an estimated 120,000 barrels per day production at peak levels. To put this in perspective – the total stage two investment of £4.5 billion is the equivalent of nine Glasgow 2014 Commonwealth Games. The value of the field is almost £300 billion.

This is a single, yet highly significant field. In the 1970s, when it was identified, it was outwith the reach of drilling companies. With advances in technology deeper drilling is now possible, which will boost tax income for an independent Scotland. Other fields off to the West of Shetland and the Atlantic are predicted to overtake North Sea production in future decades.

New oil fields exceed expectations

There has been speculation that the Clair Ridge field “far exceeds expectations”. This would make Clair Ridge – which is already forecast to continue until 2050 – proof that offshore revenue will give Scotland extra revenue far into the 21st century. Already Hurricane Energy have reported that the Lancaster field has ‘well exceeded expectations‘.

Alongside this boost to the case for independence, it’s important to note that Scotland is a wealthy country without oil. In providing at least a £1 trillion asset, the sector does provide a massive financial bonus for an independent country.

BP and its co-venturers Shell, ConocoPhillips and Chevron announced today their decision to proceed with a two-year appraisal programme to look at the possibility of developing a third phase of the giant Clair field, originally discovered in 1977, west of the Shetland Islands. The initial commitment involves a two year programme to drill five appraisal wells. This could increase to between eight and twelve wells, depending on results from these first wells. Drilling of the first well commenced recently.The objectives of the programme are to provide greater certainty on overall reservoir volumes, including their distribution and fluid characteristics; to evaluate technologies to improve recovery from Greater Clair; and to test the possibility of new standalone developments and linkages to Clair Ridge.Trevor Garlick, Regional President for BP North Sea, said: “This is a major milestone and a further big commitment to the west of Shetland by BP and its co-venturers. If successful, the appraisal programme could pave the way for a third phase of development at Clair – this is now a real possibility.”

Edward Davey, Energy and Climate Change Secretary, said: “This announcement by BP of a two year appraisal programme for the Greater Clair area West of Shetland is excellent news. It shows the industry’s commitment to maximise the potential in this area, which could hold up to 17% of our oil and gas reserves. “Greater Clair proves there is still a long future for oil and gas production in the North Sea and will give confidence to new recruits that the industry offers a career for life.”John Hayes, Energy Minister, said: “Greater Clair is extremely significant as it reinforces West of Shetland as an important area of future oil and gas development. “The Government is working extremely hard to ensure the oil and gas industry has the confidence and certainty it needs to invest, providing the UK with a source of energy security and jobs for years to come.”

The initial investment in the appraisal programme will be greater than $500 million gross.

Press Release, March 28, 2013

2 years later 3 platforms are being created,so far.

[…] he visited Shetland on an unnanounced visit that just happened to coincide with the discovery of massive new finds that went largely unreported, that Ian Wood attacked the Scottish government’s oil […]

[…] there was only five years of oil left in the entire North Sea, and ignoring stories like this one, which says that just one Oil Field in the North Sea (Clair Ridge) will be running until next […]

[…] in the strength of Scotland’s oil and gas sector. In recent months reports have focus on the new Clair Ridge field, a massive £4.5 billion oil investment […]

[…] https://www.businessforscotland.com/clair-ridge-and-scotlands-new-oil-boom/ […]

why dont the media report clair ridge findings. is mr woods assesment compatible with clair results ,

why have crews been sent home till after referendum

jmca

Upon doing some digging into the subject of the Clair Field I came across a BP article that stated they estimate the field at producing around 640 million barrels of oil. Other articles state that estimates of reserves in the field are set to be around 7-8billion barrels. At the minute from what I have read and can gather they only have the capabilities or technology to access 640 million barrels which at 100,000 estimated barrels a day equates to 17.5years of production (as stated at the minute). Does anyone know if there is anywhere that gives an insight what the future could be for the field after the initial projected 640 million barrels? Could it be another 40year wait like back in the 70s until now before the technology arises to access the rest of the oil reserves?

The current 640m barrels recoverable are extremely conservative for 8 billion barrels currently in place.

Most fields tend to get bigger as they are appraised, and technology also improves recovery.

BP are currently appraising Phase 2, and Phase 3 will follow that.

New reserve figures will be published in 2015 following the current appraisal wells, which are ‘looking good’ according to BP Chief Bob Dudley.

Then there are the reported rumours from oil workers say that results ‘far exceed expectations’.

Bob Dudley is no friend of independence, and I suspect the UK government will be encouraging them to keep a lid on things for as long as possible, given past form in playing down Scottish oil reserves.

You also have to consider that the underlying basement rock is now extremely likely to be tapped successfully, following the Hurricane Well further down the very ridge.

This could double or triple the size of the field when you look at the images.

There is already a very large oil column discovered in the Clair basement, and like the Lancaster well, it previously flowed at 2000 barrels per day with an old well in 1991, uncommercial at the time, and now reckoned to have been drilled suboptimally.

Modern seismic can more accurately steer wells in the best way to intersect larger fracture zones.

If Hurricane increased their well to 10,000 barrels/day with a modern design, then similar results are extremely likely in the far bigger Clair basement structure.

The basement is not currently included in reserves.

I suspect the Clair field will end up recovering at least 2 or 3 billion barrels.

[…] the first PM for over 30 years to do so. After his visit, workers from what is alleged to be the largest oil field in the world were sent home on full pay until after the 18th of […]

[…] https://www.businessforscotland.com/clair-ridge-and-scotlands-new-oil-boom/ […]

With regards the Clair Ridge Field.

Has anyone any documented evidence/references that the Clair Ridge will be the worlds larger oilfield?

No Clair Ridge is nowhere near the largest offshore oil field. The largest ever known field is off Saudi Arabia. Its called the Safaniyah field. Owned and operated by Saudi Aramco it consistently produces 1.5 million barrels a day. And has done since 1971!!! At peak production if they so chose, could be ramped up to 2million barrels per day!! Its on the same ridge/fault line as the biggest oil field ever known which is the Ghawar field in Eastern Saudi. It currently produces 8 million barrels a day!!! Kind of puts Clair ridge at 100,000 bpd into perspective?

Worked Sullom Voe from 1977/83. Clair field will still be producing oil 100 years from now.Moreover,Total are building an oil and gas plant next door to service up to 7 oil and gas fields in Atlantic waters.

Was on the west Phoenix and yes that’s drilling for total they expected gas but found a lot of oil in the region and are upgrading the plant to take oil and gas. Looks like they have been hitting targets

Whilst manning a YES street stall this afternoon in Callander I had an interesting conversation with a supporter from Glasgow who works for the giant oil services company Schlumberger. During a conversation about Scotland’s wealth he gave a heads up about further evidence of more very large scale oil finds in the area West of Shetland and totally unconnected to BP’s Clair field but which the company’s staff are discouraged from talking about for the time being. Perhaps someone here might have more information on specific new fields in this area which have been proved and which Westminster will be anxious to bury until after September. Better to expose now rather than see Scotland being deprived of our assets as per the 1970′s. Anyone got more information?

Chances are he was talking about the oil discovered in the firth of Clyde a few decades ago which was stopped before it was even begun thanks to the MoDs Faslane. You can find details of it via google.

– Banana Hammock

its time the YES side took off the gloves and informed the people of Scotland of this massive oil find and of the hidden truths played out by the Westminster governments in the past and present of our oil reserves and its potential financial gains for Scotland. Wake up!

I found this while reading last night. Some very detailed and highly relevant information within:

http://www.scotsindependent.org/features/game_changer.htm

Is there any way Westminster can claim that oil assets are shared assets?

I don’t think so Wilma. It’s well established that geographically fixed resources belong to the country in whose waters they are located.

In the 1974 McCrone Report:

…it is hard to see any conclusion other than to allow Scotland to have that part of the Continental Shelf which would have been hers if she had been independent all along.

It must be concluded therefore that large revenues and balance of payments gains would indeed accrue to a Scottish Government in the event of independence provided that steps were taken either by carried interest or by taxation to secure the Government ‘take’.

The line is currently the median line as defined by UNCLOS. It was moved there in 1999 but is an internal, not international boundary. The Scottish Gov. has a case (though whether they’d think it worth making is doubtful) that the boundary should be the same as the boundary between Scots and English law (which runs due East from just north of Berwick) but there is no case for it being any further North than the UNCLOS line. In any event, all the major fields are very far from any border line. There is a good BBC article on this: http://www.bbc.co.uk/news/uk-scotland-scotland-politics-20042070

The offshore borders are called Exclusive Economic Zones or EEZ:-

http://en.wikipedia.org/wiki/File:Scottish_eez.PNG

http://en.wikipedia.org/wiki/United_Nations_Convention_on_the_Law_of_the_Sea

… the same goes for Supermarkets by the way. Tesco, for example, is based in Hertfordshire and a quick look at Companies House website shows no Scottish Subsidiaries so it’s likely that Corporation tax and VAT arising from Scottish Stores is not currently separated out.

Hi Wilma.

Important question.

The short answer is no they can’t.

Long answer:

Over 90% of total tax revenue from oil and gas is generated in Scottish waters. This is ensured by the United Nations Convention on the Law of the Sea (UNCLOS). The ‘medium line’, used when oil was discovered in the 1960s and in 1999 when considering fish stocks, would also place the vast majority of reserves in Scottish waters so at least 90% of the oil being Scottish is an accepted fact and when official Government figures allot North Sea revenues to the Scottish accounts they do so on this basis.

So the UK Government already accepts that Scotland’s oil is a geographical, which aren’t shared.

Specifically it is defined in UNCLOS as the Exclusive Economic Zone

http://en.wikipedia.org/wiki/United_Nations_Convention_on_the_Law_of_the_Sea

Atlantic oil is more costly, but large fields such as Clair are far more economic, and improving technology brings down the costs per barrel.

Low salinity reservoir flushing will be used at Clair for example, and long horizontal wells could tap into the fractured basement rocks below.

This could be VERY significant following the recent Lancaster result nearby – in which basement rock further along the same ridge flowed oil from a single horizontal well at 10,000 barrels/day.

If you search Google for ‘Clair field fractured basement’ there is a link to a study by PLESS, JENNIFER,CLAIRE (2012)

Pages 95-99 illustrate the basement reservoir potential for Clair.

Some interesting quotes:

“It is the largest fractured reservoir in the UKCS”

“Current Phase-2 well plans only involve the cover sedimentary rocks (Ogilvie, 2011), but the presence of this large oil column in the basement on the ridge means that there is the potential that the basement within this area is also acting as a very significant hydrocarbon reservoir”

and

“The basement is not currently considered in any of the reservoir capacity calculations or production models within the Clair Field”

Perhaps this is what the recent excitement is about.

It seems extremely likely that BP will/has been able to replicate the Lancaster results at Clair.

And this is one field alone.

The map above is a great example of Scotland’s energy potential, with the area offshore around 6 times bigger than onshore.

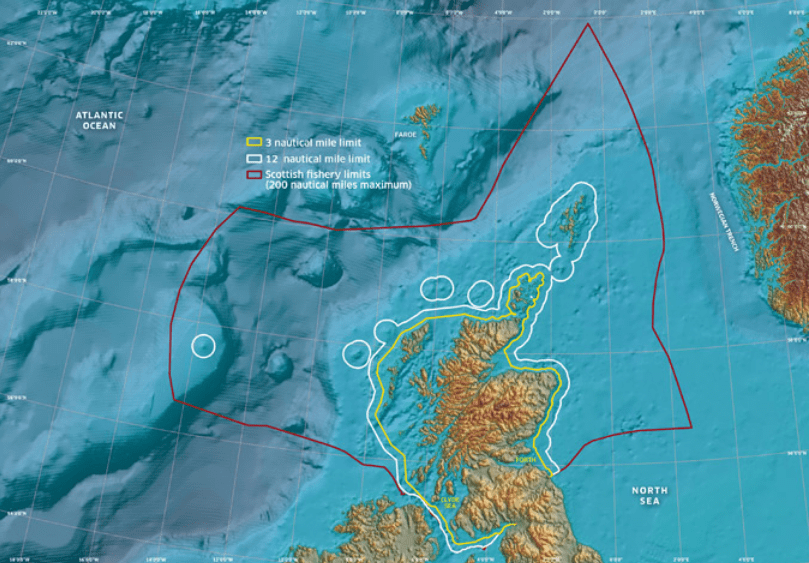

And not just oil potential, but wind, wave etc.

Perhaps after independence, we will see a national energy company set up – playing a big part in Scotland’s future prosperity.

A Scottish Statoil would be nice..

Onwards, if you look at the Hurricane Energy press release for the Lancaster sub basement discovery, it says that the 9,800 BPD figure was limited by surface equipment so actual natural flow could be a lot higher.

A view from BP: http://www.youtube.com/watch?v=kxZlMLmbgQ4&feature=share

I am reading that the Clair Ridge start-up will be delayed to 2017.

Apparently, the heavy work load in the Hyundai Heavy Industries yard has delayed fabrication of the 2 topsides units.

BP say 50% of the £4.5 billion investment will be with 80 or so UK companies.

The Jackets from Norway and the Topsides from Korea, it is a pity that we appear not to be able to have them fabricated in Scotland.

As you are aware in 2013 BP announced a 2 year initial 5 well drilling appraisal programme for the Greater Clair area, I understand they have high hopes off.

It maybe that all the recent headlines about a large oil find maybe connected with this appraisal programme, though I have not seen any evidence stating so and would not expect any given commercial considerations etc.

I would not expect results to be formally announced until the programme results are analysed, but that it for us to wonder and BP to say.

I would like to know who owns the rigs and employes the crew for the rigs and who owns the rights to the oil fields in question. What is the current taxation on each barrel of oil. Thanks , Tracy

Hi Tracy,

Full details available from HMRC here:

http://www.hmrc.gov.uk/international/ns-fiscal3.htm

Rates can be seen here:

http://www.ifs.org.uk/uploads/publications/ff/north_sea.xls

A study on total tax contribution is here:

http://www.pwc.co.uk/tax/publications/total-tax-contribution-of-the-uk-oil-gas-industry.jhtml

It’s worth noting that corporation tax makes up a large proportion and many oil companies have UK headquarters in London. Whether any of this Corporation tax currently accrues to Scotland is unclear but it is likely that after independence they would need a Scottish Headquarters and pay CT directly to the Scottish Government.

No they would not have to set up a Scottish HQ. They will pay their corporation tax in their parent country …( England )USA France as they do now.

Scotland will not see much if any corporation tax as the operators will cross charge other costs like HR / IT / Accounts making the operation run at break even. A bit like Diageo do just now through its Dutch office.

Perhaps if corporation tax was lower in Scotland they may choose to funnel profits through Scotland instead?

Hi Tracy.

Thanks for the question.

The Clair Partnership involves four major players: BP,

ConocoPhillips,Chevron Corporation and Royal Dutch Shell.

Oil taxes are applied on profits through corporation tax and for fields opened prior to 1993 through Petroleum Revenue Tax. So the tax is on profits rather than per barrel.

Further information is available here: https://www.gov.uk/oil-and-gas-taxation

I was hoping BfS would cover the breaking story concerning the Clair field’s future yield. Thank you.

Any inside information, even gossip, about Cameron’s clandestine visitations?

Hi Dan.

I was aware of some speculation online regarding developments in the Clair fields relating to Cameron’s visit.

Although I think the facts of the development speak for themselves!

Estimates are that the Atlantic Sector of Scotland’s EEZ may contain two to three times the amount of hydrocarbons that are and were in the North Sea. That would put their potential value at between £7.5 trillion and £11.25 trillion. There are trillions of tons of coal under the North Sea which has the potential to produce coalbed methane and there are substantial quantities of hydrocarbons under mainland Scotland.

Whilst I appreciate that it is currently impossible to objectively quantify these hydrocarbons that doesn’t mean that they don’t exist. Even if only a small proportion is economical to extract, I can’t help feeling that the Yes campaign are considerably understating Scotland’s hydrocarbon potential.

That’s true I dare say but Atlantic oil is much more difficult and expensive to extract.

There are a lot of myths and partial truths about the costs of oil production in the North Sea. These are used by DECC, the OBR and Better Together to try to downplay the potential benefits of the oil and gas sector to an independent Scotland.

Costs were about £3 (less than $5) per barrel in 2004 according to DECC. These costs included all production costs, all exploration costs and all capital expenditure costs. This low cost per barrel was due to the incredibly low levels of investment and higher than present production levels. These higher production levels were the result of investments made decades / years earlier. Low investment costs and higher than present production levels resulted in a much lower cost per barrel than was the case in 2012.

Production fell steeply in the first decade of this century because of very low levels of investment in the late 90s and early this century. Why was investment so low during this period? The answer is quite simple. When oil was circa $20 per barrel in the 90s it wasn’t worth investing in new production in Scotland’s EEZ. It’s not a case of oil running out. It just wasn’t as economic to invest in developing new fields with such low prices.

Since 2004, the price of oil shot up, fell back and has been relatively stable in the last few years, averaging between five and six times more than the price during the 90s. As a result, investment in Scotland’s EEZ has increased to a massive extent however it will take a number of years before these new investments come on stream.

According to DECC the cost of extracting oil from all sources was under £10 (circa $15) per barrel in 2012. This is about three times the 2004 costs. Brent Crude averaged around $110 per barrel in 2012. Extracting oil and gas was very profitable despite higher costs per barrel and costs could rise considerably before the profitability of Atlantic Sector oil would become uneconomic.

Why have costs increased so much between 2004 and 2012? There are many reasons but two of these are particularly important; unexpectedly low production levels and record high investment costs. As mentioned earlier, these costs included all production costs, all exploration costs and all capital expenditure costs. Production was low in 2012, not only because of a lack of investment in the 90s and early this century but also because of a variety of well publicised operational problems which impacted output. Investment had reached a record high because higher oil prices are making new investments very profitable indeed. These investments haven’t reached the production stage so the oil companies are incurring substantial costs without corresponding revenues. Record investment costs are therefore being spread across unusually low volumes of oil thus giving a particularly high cost per barrel.

The well publicised production problems have now been resolved and once the new investments come on stream over the next few years, investment costs could fall back somewhat. Total costs will then be spread across increasing volumes and cost per barrel may well begin to fall back. If, on the other hand, record investment levels continue it will be because of the potential for future profits. That would be good news for Scotland in the long run however the resulting tax reliefs would affect tax take and the costs per barrel in the short term.

In summary, oil currently sells for circa $110 per barrel. The cost of extraction at circa $15 or $20 per barrel gives oil companies ample profits despite the costs of record investment levels. So, whilst it is true to say that the costs of extracting oil have risen considerably in recent years, extracting oil and gas from Scotland’s EEZ is considerably more profitable than it was in the 90s when peak oil occurred.

In my previous post, I touched on the potential for oil and gas being developed elsewhere in the Atlantic Sector of Scotland’s EEZ. The reason why the sector West of Shetland is being exploited rather than the Hebrides sector is because of the proximity of the existing infrastructure and skilled labour in Shetland. Development of the Hebrides sector would necessitate costly new infrastructure linking new platforms with new shore facilities. West of Shetland is therefore the “low hanging fruit” at present.

There were reports earlier this year (e.g. in Bella Caledonia) that the world’s largest oil field lies off Lewis. If true, then perhaps the investment in new infrastructure might be justified but I expect that it will be a number of years before it is fully explored and exploited. One possibility might be an independent Scotland creating its own state oil company, along the lines of BNOC or Statoil, to develop or to facilitate and coordinate the development this sector of the EEZ.

Norway’s sovereign wealth fund has benefited not just from the taxes on hydrocarbons but also from the profits. I wonder how much different the UK’s finances would be now had the government not privatised BNOC and British Gas and sold off its majority stake in BP?

More details of Scotland’s hydrocarbon potential are in this article. It’s quite technical and could probably benefit from a good executive summary and some expert review and critique but it identifies the huge potential for hydrocarbons in Scotland’s EEZ.

http://bellacaledonia.org.uk/2014/06/11/the-real-state-of-scotlands-oil-and-gas-reserves/

Your average operating costs are biased towards the “easy” fields in England’s bit of the North Sea. Compare that with the O&G UK Activity Report :

“Whist the narrative has concentrated on average costs across the UKCS, individual field costs vary extensively. In 2012, a number of assets were seen to have operating costs of £5 per boe or less, typically located in the southern North Sea. Such fields were not however representative of the southern North Sea as a whole, where operating costs averaged £9.30 per boe. At the other extreme, a significant number of assets had operating costs in excess of £30 per boe, many of which are located in the northern North Sea. Indeed the northern North Sea remained the most expensive region, averaging at £19 per boe.”

And that’s just operating costs – in car terms it’s like looking at the cost of petrol without the cost of buying the car. Capex costs can be as much again – and if you’re looking at taxable profits you’ve got to take off central corporate costs and exploration costs. Oil companies can still make decent money but you’re overstating their profitability.

It’s also worth mentioning that costs rise dramatically once you get into deep water – something like Clair is on the limits at 140m water, but eg the North Uist well was in 1300m of water, similar to the Macondo prospect that Deepwater Horizon was drilling. Breakeven costs in deepwater Gulf of Mexico are around $60-70/bbl, deepwater Angola pre-salt is $80-90/bbl.

That claim that “the world’s largest oil field lies off Lewis” just doesn’t stand up. It seems to be the claim of one S Fisher who was involved in seismic surveys there at some stage in the past. The first thing to say is that you don’t find anything with seismic – the only proof of commercial flowing oil is by drilling. Also seismic processing is heavily dependent on computers and so has vastly improved in the last 10-15 years; many putative reservoir structures disappear when you put old seismic through modern processing. The whole “suppressing oil discoveries” thing reminds me of the claim that Thatcher fought the Falklands war because of all the oil off the Falklands. Thirty-odd years later, no oil is being produced and only one potentially commercial field (Sea Lion) has been found with reserves equal to less than 9 months of UK consumption.

Independent consultants were ascribing probabilities of 10-20% of individual wells off the Falklands finding a commercial oilfield – and that was on the basis of modern seismic and “extras” like electromagnetic surveys. The big excitement off the Falklands was the Loligo structure which on the basis of seismic was claimed to be a giant field comparable to Forties or Brent, with nearly 6 years of UK consumption. When it was drilled the reservoir was found to be impermeable so didn’t really flow, and they’d misunderstood the thermal history so most of the oil had turned to (less valuable) gas. There’s several other wells like that – there must have been over 20 wells drilled off the Falklands in the last 20 years, but there’s only Sea Lion to show for it, plus Darwin which is a smaller condensate discovery that is on the fringes of commerciality. And most of those wells have been sited using the latest in modern seismic and EM.

On the assumption that Fisher is basing his claims on seismic from the 1990s or earlier, he cannot say there IS a field off Lewis. There may well be a structure on seismic, but at this stage it has maybe a 1 in 20 chance of being a commercial oilfield and it is misleading to say that such a field definitely exists.

Just because oil has not materialised yet; doesn’t negate that the oil was why Mrs T went to war. You state that there have been many wells and exploration, so obviously there were expectations.

See Algy Cluff on coal